A handy guide to commonly-used homeownership-related terms.

A handy guide to commonly-used homeownership-related terms

A mortgage in which the interest rate changes with the market without the need to refinance.

A calculated series of monthly payments in order to pay off your fixed-rate or adjustable rate mortgage.

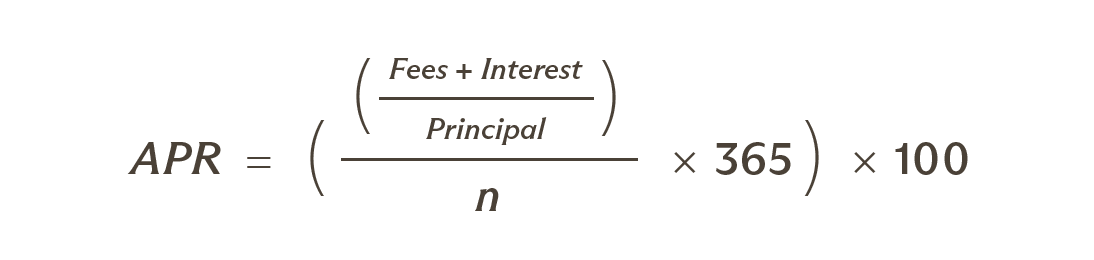

An interest rate that reflects the yearly cost of a mortgage. This rate may be higher than the initial or advertised rate because it takes discount points and other credit costs into account.

An estimated value of a property made by a qualified appraiser that incorporates market value, road maintenance, sewage and other infrastructure factors.

When a financial institution pays the remaining balance of your mortgage in exchange for equity in your home. Once the mortgage is paid off the bank will continue to make payments to the owner toward the appraised value of the home and in exchange the home will eventually be owned by the bank. When accepting this loan, the amount paid out to the owner – usually 80% of the market value minus your current mortgage balance – will be added back onto your current mortgage.

A ratio, expressed as a percentage, of a borrower's monthly payment obligations for long-term debts divided by the borrower's effective net income (for FHA/VA loans) or gross monthly income (for conventional loans). This ratio should ideally be under 50% and is the 2nd most important piece of financial info behind a borrower's FICO score.

When a homeowner's monthly mortgage payments do not satisfy the mortgage note rate, this unpaid interest is then deferred by adding it to the loan balance.

Points are fees paid to a lender in exchange for a reduced interest rate. A single point is typically sold for 1% of your total loan amount.

Fannie Mae: Federal National Mortgage Association

Ginnie Mae: Government National Mortgage Association

Freddie Mac: Federal Home Loan Mortgage Corporation

A form of credit score which takes data from Equifax, Exeprian, and Transunion. The score utilizes, among other factors: payment history, amount of relative debts, age of credit, how many types of credits and number of recent applications for credit.

A mortgage in which the interest rate is fixed at the time of the loan, this interest rate can be changed by refinancing your mortgage.

When applying for a new line of credit, lenders will check your credit history to determine any risk. This can lower your credit score for up to 12 months.

When the owner of a piece of property borrows money against the equity of that property on an as needed basis. This allows borrowers to only pay interest for money you use and not the full value of the property.

Make sure to note the fine print of your HELOC as some mortgage firms deposit the full appraised value of the house in a separate, lump-sum account which incurs interest.

A portion of a borrower’s monthly payments held by the bank to pay for taxes, hazard/mortgage insurance, lease payments or any other outstanding fees.

A penalty that is placed on a piece of property by a bank, lender, contractor or government entity until the payment or satisfaction of a debt or financial obligation to that entity. Different liens are repaid after the property is sold and in this order: tax, insurance, mortgage, and finally construction liens.

The relationship between the amount of a mortgage loan and the appraised value of the property expressed in a percentage. When applying for a mortgage or reverse mortgage it helps to have this ratio below 80%. The higher the down-payment, the lower the ratio gets.

Money paid monthly by the homeowner to insure a mortgage. Banks usually require insurance unless the borrower can put down at least 20% of the loan. Some conventional loans allow borrowers to pay their way to 20% equity in the property to stop this charge.

Occurs when a homeowners' monthly payments are not large enough to pay the interest due on the loan. This unpaid interest is then added to the unpaid balance of the loan which can cause the homeowner to end up owing more than the original balance of the loan.

Typically reserved for homeowners aged 60+, reverse mortgages allow homeowners to borrow money against the equity of their property. Borrowers receive the cash value of their home in either a line of credit, lump sum or fixed monthly payments. Federal regulations dictate this loan shall not exceed the market value of the home and becomes due when the owner dies, sells the home or moves as they are no longer the primary resident.

A loan that utilizes the property as collateral and incurs a mortgage lien on the property. This mortgage will be separate from the owner’s original mortgage on the house and will incur a separate interest charge.